Will My Credit Improve After Paying Off My Student Loans: Discuss Briefly

Feb 27, 2024 By Susan Kelly

Introduction

Student loan debt is one of the most common forms of debt. Paying off student loan debt can greatly benefit one's credit score and financial stability. It has become increasingly difficult for students to pay off their loans, and many wonder if their credit scores will improve after paying off their student loans. This article explores the answer to this question and other related issues regarding a student's credit score and loan repayment.

The Relationship Between Student Loan Debt & Credit Score

Student loan debt is one of the most common forms of debt. It can have a major impact on an individual's credit score, which affects their ability to access loans, mortgages, and other types of credit. The relationship between student loan debt and credit score is complex and often needs to be understood by borrowers. Generally speaking, having too much debt or not being able to make payments on time can damage your credit score; however, it's important to understand that there are also positive benefits associated with having student loan debt.

How Does Paying Off Student Loans Affect Credit Scores?

Paying off student loans can positively and negatively affect your credit score. On the one hand, paying off a student loan in full will immediately boost your credit score, showing that you are now debt-free. On the other hand, if you pay off a large amount of debt all at once, this can also hurt your credit score by lowering your available credit limit, which could affect your utilization rate. So it is important to weigh these factors when deciding whether or not to pay off student loans quickly or over time.

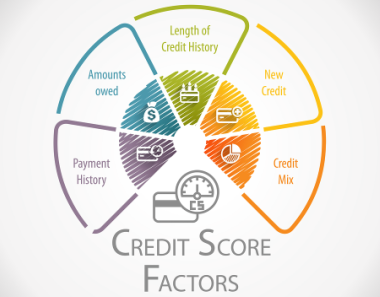

What Other Factors Affect Credit Scores After Paying Off Student Loans?

There are a variety of other factors that can impact your credit score after paying off student loans. These include payment history and credit utilization rate. A good payment history, which means you have been making payments on time for all your debts, is essential in maintaining a healthy credit score. Additionally, having a low credit utilization rate (the amount of debt you owe versus the amount of available credit) will help to keep your score high.

How Long Does It Take to See Results?

The results of paying off student loans will vary depending on the individual's situation and how they manage their finances in the future. Generally speaking, it may take anywhere from 30-90 days for the effects to be seen on an individual's credit score.

Benefits of Paying Off Student Loans for My Credit Improve

Paying off student loans can significantly impact one's credit score and financial stability. For those with good credit, paying off these loans can drastically improve their credit score. This is because paying off a loan in full, or even making consistent payments on time over an extended period, shows lenders that you are reliable and responsible with your finances. Paying off student loans can also reduce the amount of high-interest debt one carries, leading to lower monthly payments and more money in the bank.

The second benefit of paying off student loans is that it improves one's financial stability by freeing up cash for other expenses or investments. When student loan debt is paid off quickly, more income will be available each month to use as desired. This could include emergency funds, personal savings accounts, retirement savings accounts, investing opportunities, or simply enjoying life a little more.

The third benefit of paying off student loans is that it will dramatically lower the debt one carries. This can be especially beneficial for those with high balances or multiple student loans with different lenders. Having less debt overall means fewer minimum monthly payments, which in turn leads to an improvement in one's credit score, as creditors view this as an indication of financial responsibility and trustworthiness.

Finally, paying off student loan debt has the added benefit of increasing access to other forms of credit. When creditors notice that you can pay off your debts responsibly and consistently, they may be willing to offer you better terms on future borrowing opportunities. This could mean lower interest rates on new loans, higher credit limits, or lower processing fees.

Conclusion

Paying off student loans can positively affect an individual's credit score. Still, it is important to weigh the factors and understand the impact that this will have on your overall financial situation. It may take 90 days for the effects of paying off student loans to be seen in an individual's credit score, so patience is key. If managed correctly, paying off student loan debt can help improve one's credit score and ultimately lead to a more financially sound future.

Insurance Solves Three Major Things in Life

Dual Citizenship

Should I Get a 40-Year Mortgage

Unit Trust

Understanding Contractors' All Risks (CAR) Insurance: A Comprehensive Guide

A Review of Betterment’s New SmartDeposit Feature For Automatic Saving

Trading Mining Companies' Stocks

Top 3 Investments for a Roth IRA

First-Time Home Buyer Programs in New Mexico